The Future of Satellite Connectivity in MENA: Trends and Growth Areas

The Middle East and North Africa (MENA) region is witnessing a dynamic shift in satellite connectivity, driven by increasing demand across enterprise, mobility, defense, video and consumer broadband services. As digital transformation accelerates and terrestrial infrastructure remains limited in remote areas, satellite operators are stepping up to meet regional demands. With the presence of HTS and LEO satellites, the MENA market is well positioned for sustained growth amid ongoing industry changes.

ABS’s Competitive Advantage in the MENA Market

ABS’s wide-beam coverage across continents gives it a competitive edge in the region. Its footprint aligns well with MENA’s diverse geographic and regulatory environments, making it an ideal partner for enterprises, governments, and mobility clients.

ABS also leases capacity to other operators to help fill coverage gaps, unlocking additional revenue streams. While performance optimizations continue to evolve, ABS remains a relevant and dependable choice for clients needing reliable, wide-area satellite access.

1. Enterprise and Government Connectivity

Government and enterprise clients in MENA rely on satellite networks to support mission-critical operations in sectors such as energy, defense, and mining. IP trunking and VSAT services play a vital role in enabling data transmission for essential infrastructure, such as oil & gas and mining operations.

Onshore sites often present a more stable market, but regulatory requirements for satellite operators—particularly LEO providers—vary significantly across MENA. While some countries are actively enabling LEO services, many others still have pending regulatory approvals or restrictive licensing processes in place.

– EICON Report on Regulatory Approvals for Starlink Services in MENA Countries

ABS’s experience working with governments in Africa demonstrates our ability to deliver secure, reliable connectivity even in highly remote or regulated environments for our partners in the MENA region.

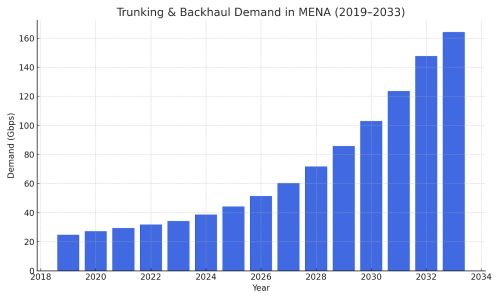

Satellite trunking and backhaul demand in MENA is projected to grow from 17.77 Gbps in 2023 to 161.69 Gbps by 2033, across both GEO and NGSO systems.

Source: Novaspace, “Satellite Connectivity and Video Markets, 2024 Edition,” Chapter 3.6: MENA Region

2. Mobility – Especially Maritime

Mobility remains one of the most demanding and fast-growing areas of satellite connectivity in MENA, particularly in the maritime sector. The region’s vast geography and critical offshore operations mean connectivity at sea is more important than ever. ABS stands out with its unique beam coverage across continents, enabling us to meet mobility requirements in ways that even major providers may not.

With three out of five GEO satellites covering MENA, ABS delivers consistent and cross-regional coverage that is highly valued by partners requiring uninterrupted service across vast distances. ABS’s coverage advantage ensures dependable connectivity where it matters most.

Land mobility is also significant, especially with the rise of connected emergency vehicles, smart fleets, IoT, and satellite-5G integration. ABS supports IP trunking and VSAT applications over C- and Ku-bands. With our teleport presence in Cyprus, we are well-positioned to provide coverage across the entire MENA region.

HTS NGSO trunking/backhaul demand in MENA is projected to grow from 0.82 Gbps in 2023 to 139.02 Gbps by 2033.

Source: Novaspace, “Satellite Connectivity and Video Markets, 2024 Edition,” Chapter 3.6: MENA Region

The Rise of GEO and NGSO HTS Capacity

MENA is becoming a hotspot for HTS investment, with both GEO and NGSO satellites playing complementary roles. NGSO satellites, especially LEO, are favored for low-latency, real-time applications like mobility and cloud access, while GEO satellites continue to serve as the backbone for long-term, high-capacity needs in government, corporate and broadcast use cases.

Multi-orbit strategies are gaining popularity, enabling operators like ABS to combine GEO and NGSO assets for improved efficiency and flexibility.

GEO HTS trunking/backhaul demand is expected to rise from 16.95 Gbps in 2023 to 22.67 Gbps by 2033.

Source: Novaspace, “Satellite Connectivity and Video Markets, 2024 Edition,” Chapter 3.6: MENA Region